Date: 12 August 2025

The Bank Holiday Trap: The Hidden Cost of Hospitality

With the August Bank Holiday (August 25th) fast approaching, the “Shed-Proprietor” community—those individuals and companies who have invested in high-spec, permanent garden office structures—is currently divided. The temptation to leverage the multi-purpose nature of these insulated pods is exceptionally high. Specifically, the idea of installing a high-end sofa bed or converting the office into a temporary annex to host family for the long weekend is a common discussion point, especially given that UK hotel prices are currently at an all-time peak, making alternative accommodation a costly proposition.

However, from a Her Majesty’s Revenue and Customs (HMRC) perspective, that seemingly innocent extra pillow could be the most expensive luxury you ever afford. The core issue revolves around the strict definition of “exclusive business use” and the resulting tax implications for assets funded by a company.

The 2025/26 Enforcement: The Benefit in Kind (BIK) Trigger

The 2025/26 tax year has ushered in a renewed and rigorous focus on “Benefit in Kind” (BIK) enforcement, particularly concerning high-value assets like garden offices. If the construction and running of your garden office were paid for or subsidised by your business, and you then use it for any non-business purpose—even briefly, such as a single weekend of hosting—you immediately trigger a BIK charge.

This charge is not based on the actual time the office was used for personal reasons, but on an annualised percentage of the asset’s value. The current statutory rate for BIK on company-owned assets made available for private use is based on 20% of the market value of the asset (the garden office structure itself), plus the full cost of any annual running expenses (e.g., heating, lighting, internet) absorbed by the company.

The 15% NI Sting: A Double Tax Burden

Compounding the personal tax liability is the recent adjustment to Employer National Insurance contributions. Under the new Budget rules implemented in April, Employer National Insurance on BIK has significantly risen to 15%.

Consider a tangible example: For a high-specification garden office valued at £50,000, a casual weekend of hosting could technically result in an annual BIK assessment of £10,000 (20% of the market value). This £10,000 is then added to the employee’s taxable income. Furthermore, the company faces an Employer National Insurance charge of £1,500 (15% of the £10,000 BIK). This calculation demonstrates how a minor deviation from the exclusive use rule can create a substantial, avoidable tax and National Insurance burden for both the employee and the business.Capital Gains Tax (CGT) vs. Business Expense Claims

Beyond the immediate BIK and NI charges, the decision to allow non-business use critically impacts the long-term tax treatment of your main residence upon sale.

The concept of “exclusive business use” is the only absolute shield protecting your home’s Principal Private Residence (PPR) relief on the garden office footprint.

- 100% Exclusive Business Use: If the garden office is used solely for work, you gain the ability to claim 100% of the build cost as a business expense, including access to Capital Allowances on fixtures and fittings. However, this use restricts your PPR relief on the proportionate footprint of the office, potentially triggering a Capital Gains Tax liability when the main house is sold.

- Dual-Use (Guest/Office): If you use the office as a guest room or for any significant personal use, you generally protect your PPR relief (as the office is no longer deemed exclusively commercial). However, this protection comes at the cost of losing the ability to claim 100% of the build as a business expense and drastically limits Capital Allowances and VAT reclamation. The tax benefits of ownership are pro-rated, and the BIK charge is triggered if the company paid for the asset.

Dual-Use Tax Comparison Table: The Trade-Off

The following table summarises the critical trade-offs facing a company-funded garden office owner:

| Feature | 100% Exclusive Business Use | Dual-Use (Guest/Office/Gym) | Implication |

| Capital Allowances | Claim fixtures/fittings only (AIA may apply). | Limited/Pro-rata only, based on business use. | Significant reduction in immediate tax relief. |

| VAT Reclamation | 100% (if company is VAT registered). | Pro-rata (e.g., 70% business use) & complex calculation. | Reduced recoverable input VAT. |

| CGT (On Sale) | Restricts PPR Relief on office footprint. CGT may apply. | Protects PPR Relief (mostly). CGT less likely. | The long-term CGT vs. immediate tax relief dilemma. |

| BIK Charge (If Co. Owned) | Zero, provided use is truly exclusive. | 20% of market value + running costs (annualised). | Creates a substantial and avoidable tax/NI cost. |

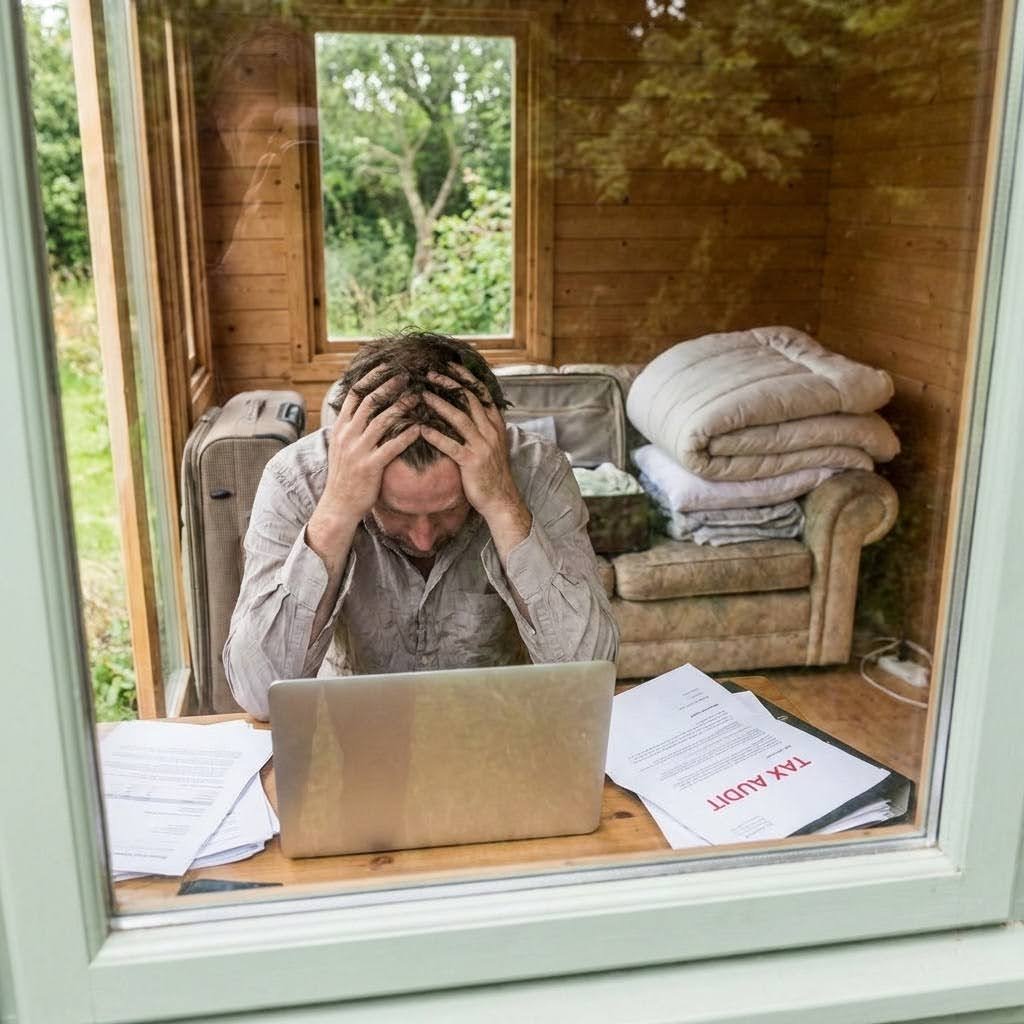

The “Incidental” Anecdote: HMRC’s Scrutiny

The concept of “incidental” personal use holds little weight under a focused HMRC audit. Tax officers are trained to look for evidence of non-exclusive use.

“Speaking with a consultant in Surrey who was audited last month. The central issue was his company-funded garden office. HMRC found a Playstation 5 gaming console and a packed-away guest duvet in his office cupboard during a site visit. They ruled the space ‘non-exclusive’, arguing that the presence of gaming gear and guest bedding demonstrated private use was intended, resulting in a back-dated tax bill of £8,000for previous tax years. He’s now cleared out all non-essential and non-business items, removed the gaming equipment entirely, and implemented a strict ‘No Guest’policy, complete with signed documentation, to robustly protect his 2025/26 ‘exclusive business use’ status.”

The lesson is clear: for maximum tax efficiency and to avoid the BIK trap, the garden office must be treated as a dedicated, sterile business environment, completely separate from the domestic sphere.

Last updated: 26 March 2026